Are you new to saving for retirement as a solopreneur or small business owner with no employees?

Then you may have heard about the solo 401(k), aka the Solo-K, Uni-k, or One-participant k, and desperately wanted to ask your business colleagues what they were talking about, but couldn’t bring yourself to ask.

I get it. In the business world, we all want to appear as successful and financially sound as possible.

Today, you’re in luck because I’m going to show you everything you need to know about the Solo 401(k) but were afraid to ask, including how to differentiate it from its most popular alternative, the SEP IRA.

There are other types of retirement accounts that business owners may choose among, too, but those will not be featured in this article.

See: SIMPLE IRA, Traditional IRA, Roth IRA, or a defined benefit plan.

You'll be ready to decide which type of retirement account is best for you as a solopreneur or small business owner.

What is a Solo 401(k)?

I'm not here to bury the lead; in simple terms, it’s a traditional 401(k) plan covering a business owner with no employees, or that person and her spouse. A 401(k) plan is a tax-advantaged retirement savings account which means that you can, even as a self-employed person, set aside money to invest for your future on a pre-tax basis.

The Solo 401(k) aims to allow the business owner to have a high savings potential, to allow the business owner to choose their tax advantage by selecting a Roth or Traditional Solo 401(k), and to save efficiently for retirement.

It also allows you to include your spouse in your plan so you both can save well for retirement as a self-employed person.

Want to know how to use the Solo 401(k) to your best advantage?

Download the Flowchart: Should I Set Up A Traditional 401(k) For My Business?

Why is the Solo 401(k) Important?

You may come across people in financial planning who believe SEPs are the best account for small business owners who have no employees a.k.a. solopreneurs.

However, the Solo 401(k) is generally considered to be better because it offers additional features and more favorable savings and investing nuances to a sole proprietor. These features include employee deferrals, catch-up contributions, and loan provisions.

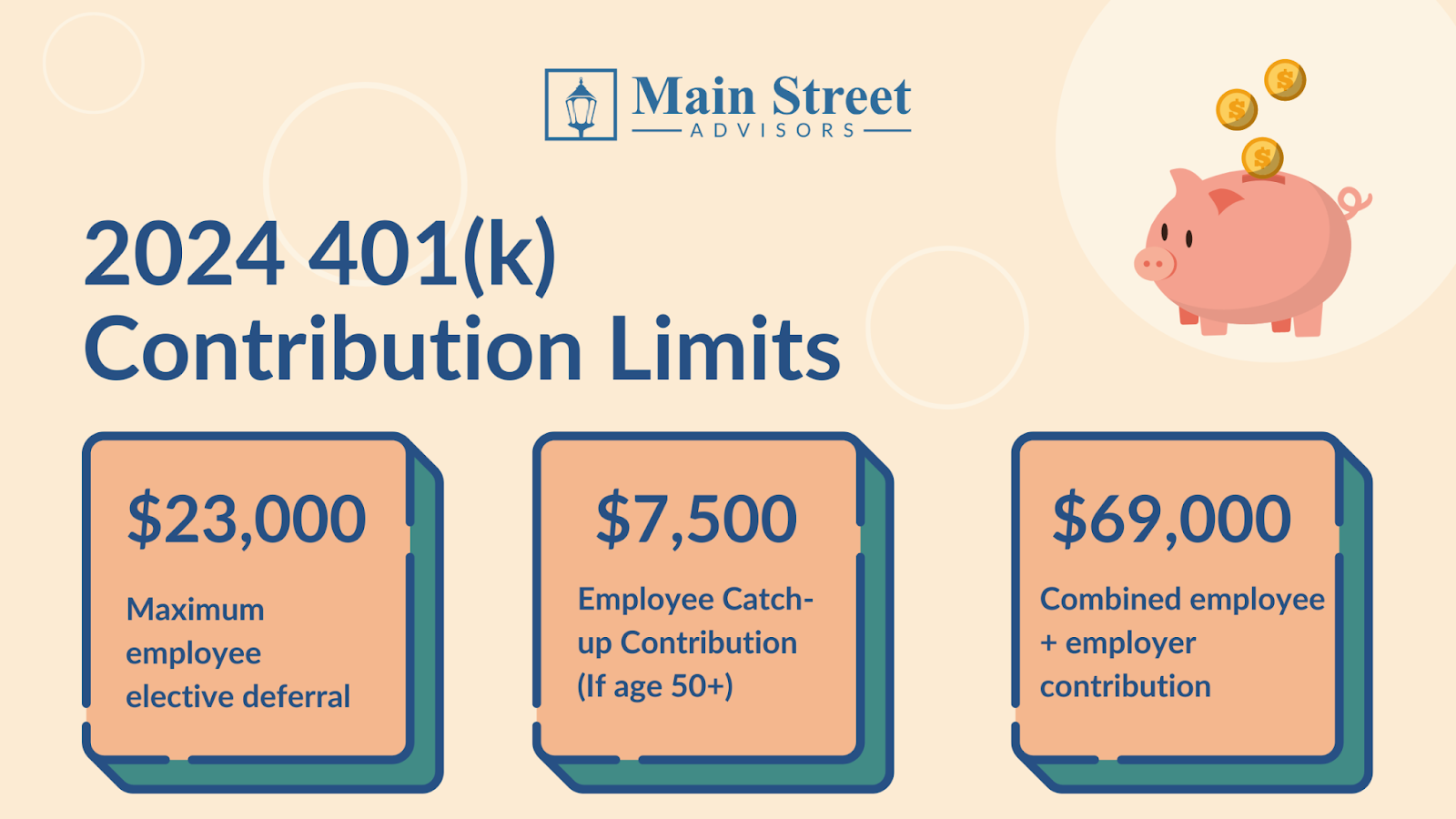

This means that unlike a SEP IRA, a solo 401(k) allows both employee and employer contributions, allowing the proprietor to contribute up to $23,000 to their own plan in 2024 even if the business is not profitable.

Like the SEP, a solo 401(k) will allow the same annual amount of $69,000 in 2024 to be contributed by the owner, but it also allows those age 50 and older to contribute an additional $7,500 as a catch-up contribution.

And the loan provision means that you are permitted to take a loan of up to the lesser of 50% of the plan balance or $50,000. I hope that you might never need to be in the position to take a loan from your 401(k), but the flexibility is a huge benefit for owners of 401(k) accounts.

When you choose the solo 401(k) you’ll be able to have a great deal of control over how your taxes this year might look based on how you choose to contribute to it.

On top of that, you’ll be better positioned to have options and flexibility when it comes to your retirement plan.

For example:

Plant Parenthood is a business owned by Lia, and she has no employees. This year, 2024, she anticipates a profit of $100,000. With a SEP, she could only contribute 20% of those business profits as the employer. If she chose a solo 401(k), she could contribute up to $23,000 as an employee and 20% of business profits as the employer.

(*20% of business profits be less than $20,000 due to self-employment taxes for both the SEP IRA and the solo 401(k) options.)

The SEP may become the retirement account of our parents’ generation and will make was for the better, more efficient Solo 401(k).

Background of the Solo 401(k)

Don't worry, this is not some boring AP history class. It might be “worse” because we are talking about the law and IRS provisions unless you love to contextualize things in history like I do!

The Solo 401(k) plan is an IRS approved plan that was initially established into law in 1962. The passing of EGTRRA in 2001 greatly enhanced it, and now it’s the most popular retirement plan for the self-employed or business owner with zero employees.

In 2001, EGTRRA said that the solo 401k could allow for employer and employee contributions, changing the numbers for how much a business owner could set aside, surpassing the SEP for how much could be contributed in a given year.

In 2010 the introduction of the Backdoor Roth IRA made the SEP IRA less desirable due to pro-rata rules that do not apply to the solo 401(k).

Inertia has real implications, though. The SEP IRA has been so popular for years, and it’s so user-friendly, that most professionals just kept suggesting that.

Then, in 2019, the SECURE Act changed the deadline to establish the solo 401(k) for employer contributions.

Check out the history over here.

How the Solo 401(k) Works

So far, we've stayed pretty theoretical in our exploration of the solo 401(k), and if you're still confused, I don't blame you.

Luckily, the solo 401(k) is more complex in theory than in practice.

I've put together a few examples of Solopreneurs with their Solo 401(k) below to help you better understand and consider whether it might be a worthy path for your own wealth building and retirement planning.

Example #1: Molly the Consultant

Molly is a consultant who gets paid as a 1099. She created a business entity years ago and has been filing taxes as an S-Corp since.

She says, “I had been using only a Roth IRA for my retirement accounts, and that’s great, but it just isn’t nearly enough to save for the future I want. Opening a Solo 401(k) was simple, and I like the control I have when it comes to saving pre-tax or post-tax. It also has flexibility for me and will accommodate the years that are really good as well as those that are leaner.”

This means that she can adjust her savings based on revenue each year.

Want to ask about your particular situation to learn if this is right for you, too? You're in luck because I have just opened up my calendar.

Example #2: Tom, the High Income Solopreneur

Tom is a high income S corp owner. And just by finishing up a financial plan for him and finding the optimal salary he can:

- Maximize his QBI (50% of wages in this case)

- Max his solo 401(k)

^In this case, Tom was able to lower his income tax liability by $75,000* with just these two crazy good money moves.

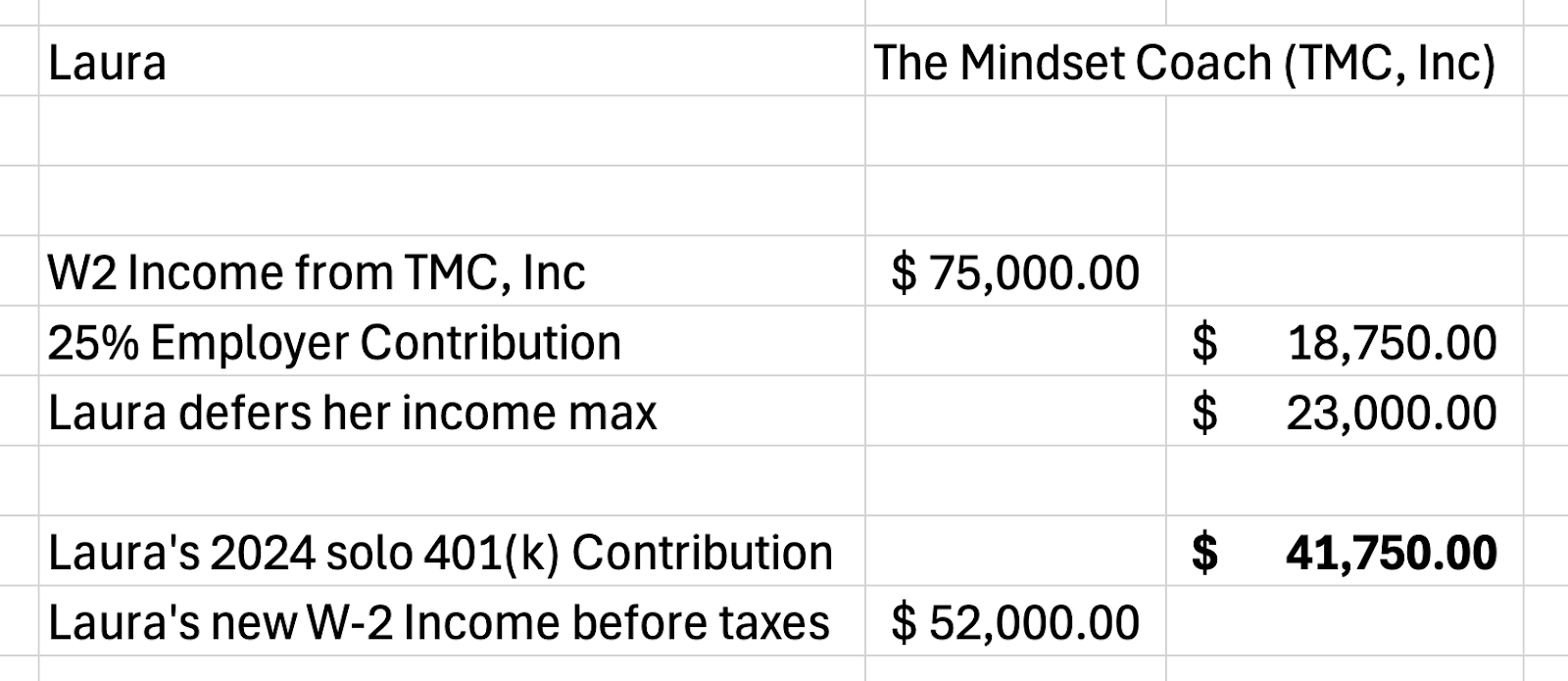

Example #3: Laura, the Mindset Coach

Laura will earn $75,000 in W2 wages from her S Corp, Mindset Matters, in 2024. She will defer $23,000 to her plan as an employee. Her business will contribute 25% of her salary to her plan: $18,750.

Total Contributions in 2024: $41,750

This is the maximum she can put into her solo 401(k) plan this year.

Explainer Video Time: Solo 401(k)

Still not sure you get the Solo 401(k) well enough to know whether it’s for you? We all learn in different ways.

Check out this video to see if it helps you out:

I hope the Solo 401(k) is crystal clear to you now.

I first launched this blog because there were really important nuances in personal finance for solopreneurs that even I didn’t fully get—being a solopreneur for years, becoming a CERTIFIED FINANCIAL PLANNER®, and even growing up in a house of business owners and a financial planner.

Do you still have questions? No shame in that! You can contact me here or find me on Facebook, X (formerly known as Twitter), and LinkedIn, where I'm always happy to answer any questions.

One thing you can do to get started with getting great at money, whether you’re ready to start your solo 401(k) or not is grab this flowchart: Should I Set Up A Traditional 401(k) For My Business?

Click here to access it now >>

Free Guide: Should I Set Up A Traditional 401(k) For My Business?